Need help? Chat with us on WhatsApp.

Zerodha deducts Tax Deducted at Source (TDS) from your trading profits as per Section 195 of the Income Tax Act, 1961. The TDS calculation depends on the type of income you generate through your trading activities.

If you have a Non-PIS account, Zerodha deducts TDS from two types of income:

- Capital gains: Income from equity delivery trades (buying and selling stocks for delivery)

- Business income: Gains from intraday equity and F&O are categorised as business income, where intraday gains are classified as speculative business income and F&O gains as non-speculative business income.

You will receive a detailed statement via email showing the computation of your gains or losses, TDS deducted, and any losses carried forward.

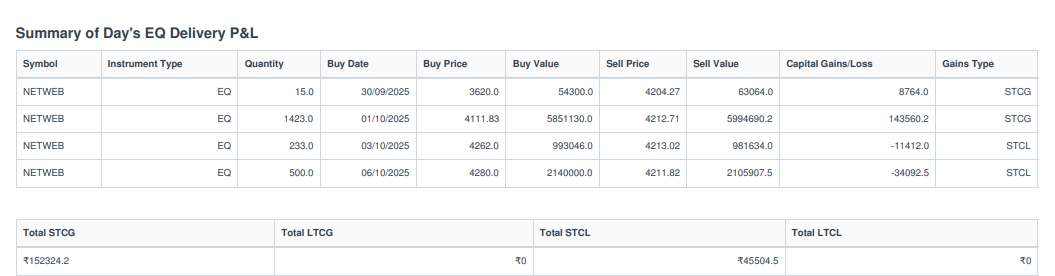

Income from your capital gains (Equity)

When you sell stocks from your Non-PIS account, Zerodha calculates capital gains based on how long you held the shares and deducts TDS accordingly.

Tax rates for capital gains

|

Segment |

Capital gains type |

Holding period |

Tax rate |

Surcharge |

Cess |

Effective rate |

|

Equity |

STCG |

Less than 365 days |

20% |

15% |

4% |

23.92% |

|

Equity |

LTCG |

More than 365 days |

12.5% |

15% |

4% |

14.95% |

|

Non-Equity |

STCG |

Less than 2 years |

30% |

15% |

4% |

35.88% |

|

Non-Equity |

LTCG |

More than 2 years |

12.5% |

15% |

4% |

14.95% |

Short-term capital gains (STCG)

Zerodha applies STCG of 23.92% on profits you make from selling stocks held for less than 365 days.

How Zerodha deducts STCG:

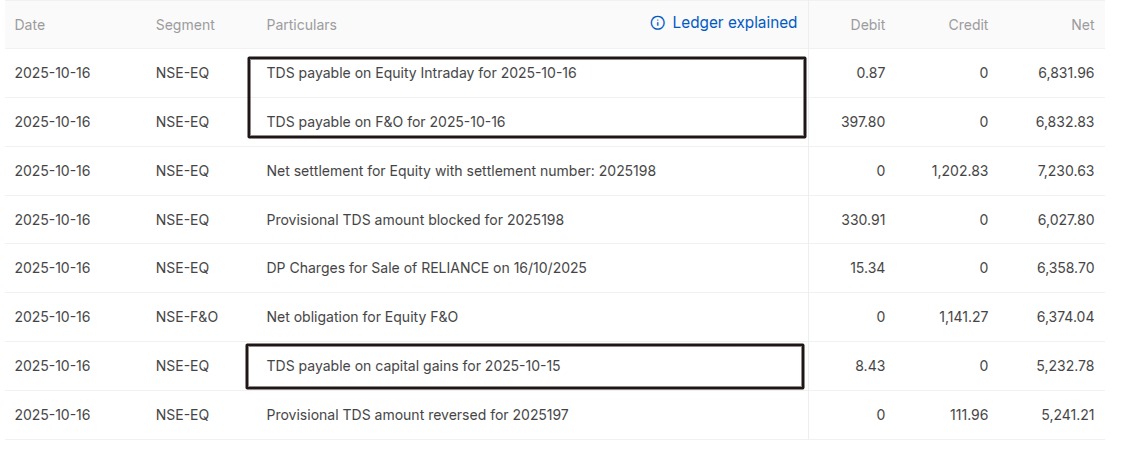

- When you sell shares, Zerodha posts a provisional TDS entry on your ledger at the end of the trading day at 20% plus cess (calculated on the amount you receive from the sale).

- At the end of the next working day (T+1), Zerodha reverses the provisional TDS and debits the actual TDS if you have made a capital gain.

Example:

- 1st April 2023: You buy 100 Reliance shares at ₹1,000 per share (total: ₹1,00,000)

- 30th May 2023: You sell them at ₹900 per share (total: ₹90,000) — Loss of ₹10,000

- 31st May 2023: You buy 100 Reliance shares again at ₹900 per share (total: ₹90,000)

- 30th June 2023: You sell them at ₹1,100 per share (total: ₹1,10,000) — Profit of ₹20,000

Zerodha deducts STCG TDS at 23.92% on the ₹20,000 profit, which equals ₹4,784.

Since you initially lost ₹10,000 and then made a profit of ₹20,000, your net gains for the financial year are ₹10,000. The applicable TDS after adjusting for the loss is ₹2,392.

Long-term capital gains (LTCG)

Zerodha applies LTCG of 14.95% on profits above ₹1,25,000 when you sell shares held for more than 365 days. Zerodha does not consider the grandfathered effect when calculating TDS on LTCG.

Zerodha cannot provide the ₹1,25,000 exemption because you may have additional capital gains through mutual funds or accounts with other brokers.

If you do not accrue any LTCG, you can claim the TDS when filing your tax returns. Contact a tax consultant or Chartered Accountant for tax-specific queries.

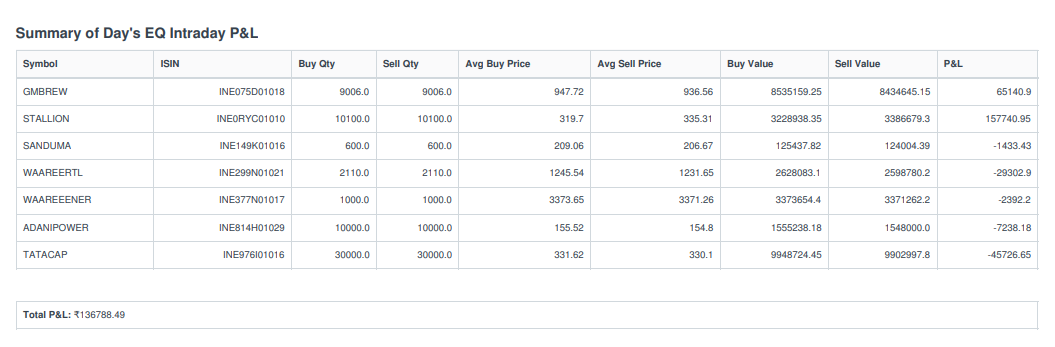

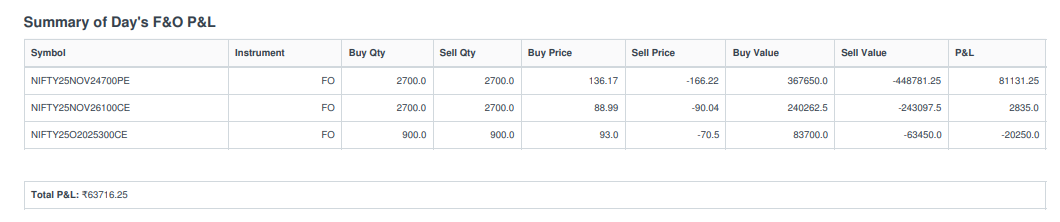

Income categorised as business (Intraday, F&O)

When you trade in Futures and Options or equity intraday, Zerodha calculates your gains at the end of each trading day and deducts TDS from your trading account if you have made any profits. This income is taxed according to the applicable income tax slab rates.

Tax rates for business income

TDS for F&O and equity intraday gains is 30% as per Section 195 of the Income Tax Act. The effective rate varies according to your income slab:

|

Income slab |

Tax rate |

Surcharge rate |

Cess (4%) |

Effective rate |

|

Up to ₹50 lakhs |

30% |

0% |

4% |

31.20% |

|

₹50L – ₹1 crore |

30% |

10% |

4% |

34.32% |

|

₹1 crore – ₹2 crore |

30% |

15% |

4% |

35.88% |

|

₹2 crore – ₹5 crore |

30% |

25% |

4% |

39% |

|

Above ₹5 crore |

30% |

37% |

4% |

42.74% |

Speculative business income

Section 43(5) of the Income Tax Act 1961 defines a speculative transaction as a contract settled without actual delivery of the underlying asset. Intraday trades are considered speculative trades, and the income or loss from these is classified as "speculative business income."

Non-speculative business income

You earn non-speculative income from business activities that are not considered speculative. Trading in F&O on recognised stock exchanges is specifically classified as non-speculative business income under the Income Tax Act.

How Zerodha deducts TDS

Zerodha deducts TDS when you make gains in either Futures and Options or equity intraday trading.

Example:

If you earn an intraday profit of ₹50,000 and an F&O profit of ₹30,000, Zerodha deducts TDS as follows:

|

Trading type |

Profit/loss |

TDS rate |

TDS deducted |

|

Intraday (EQ) |

₹50,000 profit |

31.20% |

₹15,600 |

|

F&O |

₹30,000 profit |

31.20% |

₹9,360 |

|

Total TDS deducted |

|

|

₹24,960 |

Zerodha posts these TDS entries separately in your Console ledger and sends a detailed statement to your registered email address.

Loss set-off and carry-forward rules

Income tax laws allow you to adjust losses strategically:

- You can set off non-speculative losses (F&O) against both non-speculative AND speculative business gains

- You can ONLY set off speculative losses (Intraday) against speculative gains

Example of loss carry forward:

Day 1: You make an intraday loss of ₹50,000 and earn an F&O profit of ₹30,000

|

Trading type |

Amount |

Action |

|

Intraday (EQ) |

₹50,000 loss |

Carried forward |

|

F&O |

₹30,000 profit |

TDS: ₹9,360 |

Day 2: You earn an intraday profit of ₹70,000 and an F&O loss of ₹20,000

|

Trading type |

Amount |

Adjustment |

|

F&O |

₹20,000 loss |

Available for set-off |

|

Intraday (EQ) |

₹70,000 profit |

TDS: ₹0 (see calculation below) |

Set-off calculation:

- Intraday profit: ₹70,000 (Day 2)

- Minus F&O loss from (Day 2): ₹20,000

- Minus carried forward intraday loss: ₹50,000 (Day 1)

- Net taxable profit: ₹0

- TDS deducted: ₹0

Tax statements/capital gain statements

Zerodha sends you a statement that provides a detailed computation of your gains or losses from capital gains, intraday, and F&O trades. The statement contains three sections:

1. Summary of profit and loss (P&L)

This section presents a detailed breakdown of your realised profits and losses for the day. Capital gains, intraday, and F&O trades are shown separately, with clear classification of gains and losses.

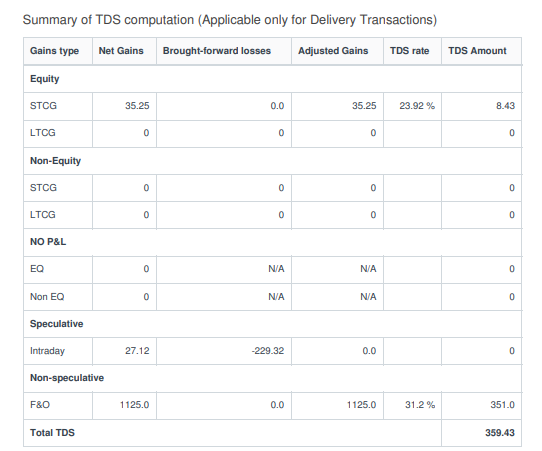

2. Summary of computation of TDS

This section summarises your net gains or losses for each income type (capital gain, intraday, and F&O trades), along with:

- Brought-forward losses: Losses carried forward from previous days

- Adjusted gains: Gains after adjusting for brought-forward losses (this represents the taxable amount)

- TDS rate and amount: The applicable tax rate and the computed TDS on taxable gains

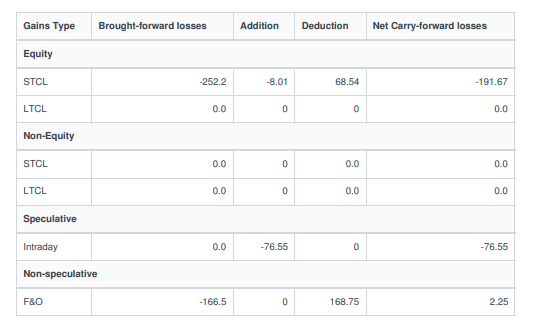

3. Summary of carry-forward losses

This table shows the opening balance of brought-forward losses. Depending on the day's profit or loss, Zerodha updates this balance as follows:

- Losses you book during the day are added to the brought-forward losses and carried forward to the next day

- Losses you set off against profits are deducted

- The resulting net figure is carried forward to the next trading day

Did you know?

- You can carry forward losses, but you cannot carry forward profits. This means if you earn a profit first and incur a loss later, the TDS already deducted cannot be reversed. However, you can claim the excess TDS when filing your income tax return

- Losses can be carried forward and set off against future profits within the financial year. As a taxpayer, you can carry forward losses for up to 8 years in the case of Capital Gains and Non-Speculative Business Losses, and up to 4 years for Speculative Losses, provided the income tax return is filed within the due date.