As per regulations, effective from 7 October 2024, Zerodha credits 100% of the proceeds from selling holdings to your trading account and makes them available on the same day for all trades, including stocks and F&O positions.

Previously, only 80% of proceeds were available for further trades on the same day, with the remaining 20% available the next day. For example, selling shares worth ₹1,00,000 would provide ₹80,000 to use on the same day and the remaining ₹20,000 the following day. Now, you can use the entire ₹1,00,000 to place trades on the same day.

SEBI requires brokers to collect margins from you before executing orders to cover potential losses. A margin shortfall occurs when you fail to maintain adequate margins. The margin shortfall is the difference between the margin SEBI requires and the available margin in the form of funds or collateral. Several factors can affect the margin amount needed for a trade, including liquidity, volatility, time to expiry for futures and options contracts, and other positions in your portfolio.

You can check the margin required to enter a trade on the order window.

Even after your order executes, the margin required for your open positions can still change. You can track the breakup of your funds balances and margin utilised on the Kite funds page.

Exchanges require the margins for all trades to be collected upfront for both F&O and equity trades. To learn more about upfront margin, visit Changes in margin requirements from 1st September 2020. The following are typical scenarios that may cause a margin shortfall and subsequent penalties:

Equity

- Intraday trade is not squared off

If you cannot square off an intraday trade, it can result in a buy or sell delivery obligation. For sell obligations where you have no holdings, an auction settlement and associated penalties may occur. To learn more, see What is short delivery and what are its consequences?

If you have a buy delivery obligation and an insufficient balance to take delivery, the broker may close your position. This could lead to a margin shortfall if your available funds are insufficient to cover both the initial trade's margin requirements and the next day's square-off transaction.

F&O

- Increase in margin requirement due to shuffling of positions

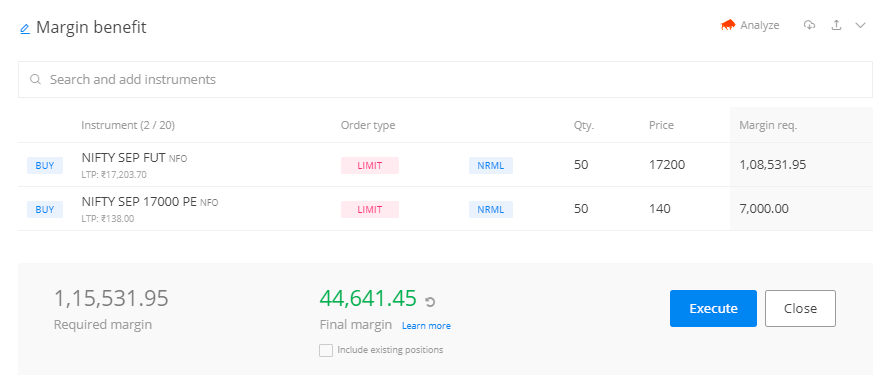

The margin requirements for F&O trading are based on SPAN and Exposure margins. The SPAN margin is calculated on your overall F&O positions held, and certain positions that reduce portfolio risk may lead to a lower margin requirement. However, if you close these positions without closing other open trades, the margin requirement can increase.

For instance, buying one lot of NIFTY futures and one lot of NIFTY put option of 17000 strike price had a margin requirement of ₹44.64 thousand. But if you square off the put option before exiting the futures trade, the margin requirement can increase to ₹1.08 lakhs, resulting in a margin shortfall if you do not have enough funds in your Zerodha account.

- Incremental physical delivery margins not maintained

In the past, exchanges settled F&O positions that were held until expiration in cash based on the underlying stock price. From October 2019, the settlement process involves giving or taking delivery of the actual shares. If you purchase option contracts, you do not need to maintain SPAN and exposure margin in your account since the margin requirement is limited to the value of the option, as the risk is also limited to that amount.

However, exchanges now settle in-the-money (ITM) options by delivery of the underlying shares due to physical delivery rules. The exchange levies physical delivery margins from four days prior to expiration for ITM options as a percentage of the applicable margins (VaR + ELM + Adhoc) of the underlying stock:

| Day (Beginning of the day) | Margins applicable |

| E-4 Day (Wednesday BOD) | 10% of VaR + ELM + Adhoc margins |

| E-3 Day (Thursday BOD) | 25% of VaR + ELM + Adhoc margins |

| E-2 Day (Friday BOD) | 45% of VaR + ELM + Adhoc margins |

| E-1 Day (Monday BOD) | 70% VaR + ELM + Adhoc margins |

To learn more about the physical settlement, visit zerodha.com/varsity/chapter/quick-note-on-physical-settlement-2

Both Equity and F&O

- End of Day (EOD) margins are not maintained

Exchanges release margin files several times a day, with the final file published in the evening reflecting any movement in the instrument during market close hours. The exchange updates the End of Day (EOD) file with the latest margins. Kite displays the margin requirement based on the most recent exchange file available, meaning it can change after market hours based on the EOD file.

To avoid a margin shortfall, keep sufficient funds in your Zerodha account above the margin requirement. A buffer of 5% is sufficient on most days if there are no significant price changes.

2. Expiry or exit of one of the leg in a hedged position

If you are holding a hedged position and one of the legs expires or you exit it, this may lead to an increase in the overall margin requirement. If you do not exit the hedged positions properly or one of the legs expires, the margin requirement increases as the margin benefit goes away due to the expiry or exit of one leg of the hedged position. This causes a margin shortfall in your account. To avoid a margin shortfall, always exit the position with the highest margin blocked first.

Penalty structure

The exchange charges a margin penalty on the shortfall amount (difference between the margin available and the margin required) at the following rates:

| Shortfall amount | Penalty Percentage |

| (< Rs 1 lakh) And (< 10% of applicable margin) | 0.5% |

| (= Rs 1 lakh) Or (= 10% of applicable margin) | 1.0% |

If your shortfall continues for more than 3 consecutive days, the exchange applies a penalty of 5% on the amount for each subsequent instance. Similarly, if you have more than 5 instances of margin shortfall in a month, the exchange charges a penalty of 5% of the shortfall amount beyond the 5th day.

The exchange charges GST at 18% on the entire penalty amount.

To learn more, visit www1.nseindia.com/products/content/derivatives/equities/penalties.htm.