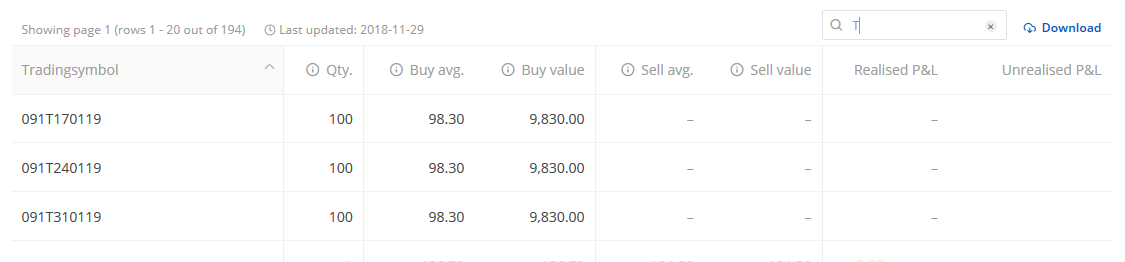

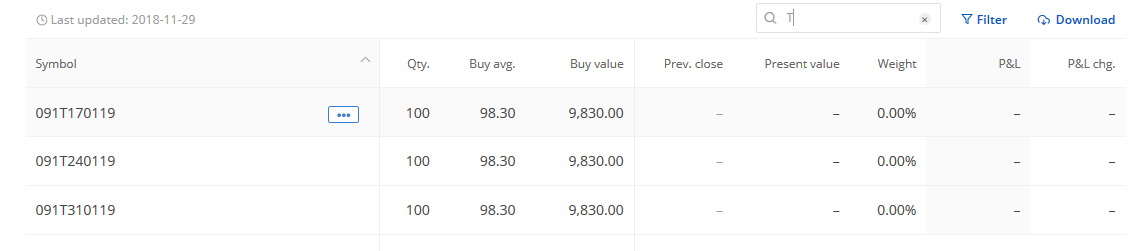

Until the maturity date, your P&L report will not display any values for:

- Sell Average

- Sell Value

- Realised P&L

- Unrealised P&L

Upon maturity, the face value of ₹100 will be considered as your selling average. Based on this, your sell value and realised P&L will be calculated.

Example scenario

- You bought 300 units of 91-day T-bill at ₹98.3. Upon maturity, your sell value will be considered as ₹100. Your profit will be ₹1.7 (₹100 - ₹98.3) × 300 units = ₹510.

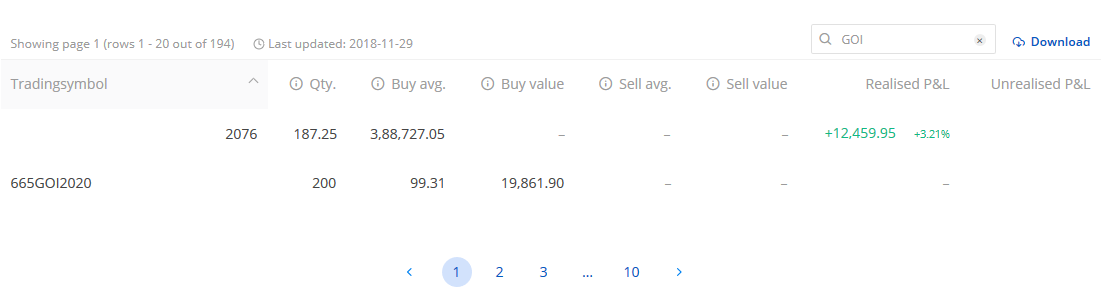

- You bought 200 units of G-secs at ₹99.31. Upon maturity, your sell value will be considered as ₹100. Your profit will be ₹0.69 (₹100 - ₹99.31) × 200 units = ₹138. The interest payments you receive will not be considered part of the P&L report.

To understand how returns are calculated, see

How are returns on G-secs calculated?